Who will bear the risks for the First-of-a-Kind (FOAK) Nuclear Power Plant in Indonesia?

In the latest draft of Indonesia’s national energy policy (KEN) and its roadmap, the introduction of a nuclear power plant (NPP) is scheduled for 2032. In... Read more.

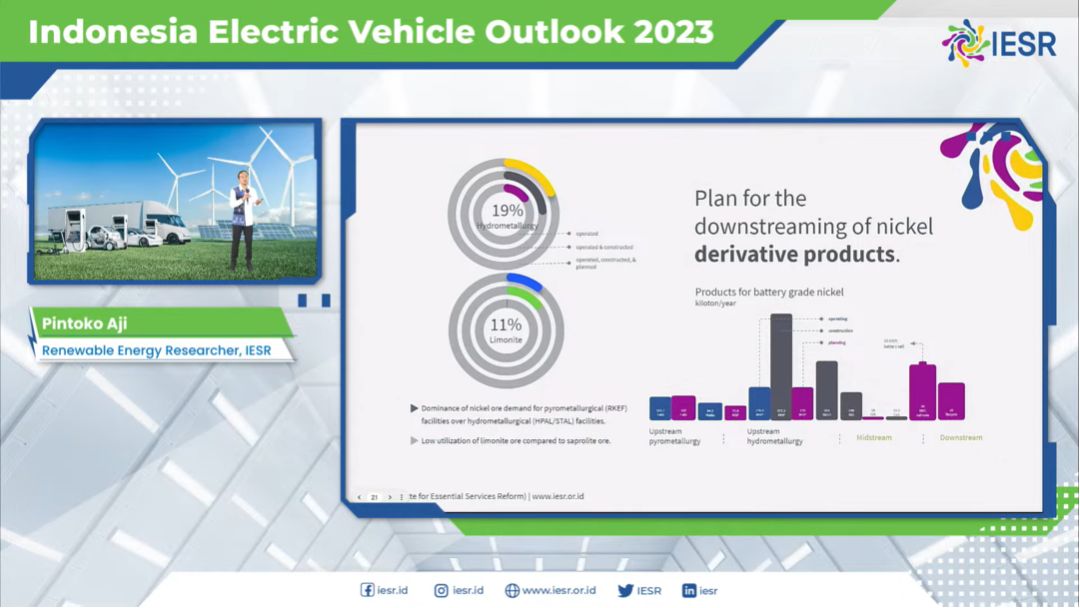

Tracking the Advancements of Indonesia’s Electric Vehicle Battery Industry

Over the present decade, the popularity of electric vehicles (EVs) has witnessed a significant increase with year-over-year sales showing exponential growth. Ac... Read more.