Jakarta, December 5, 2025 - The Institute for Essential Services Reform (IESR) notes that the world is rapidly shifting toward a low-emission economic system. In 2025, global investment in renewable energy, electricity grids, and batteries reached USD 2.2 trillion, double the amount invested in fossil fuels. Beginning January 2026, the European Union will also enforce…

Jakarta, December 4, 2025 – Although Indonesia has issued the Ministerial Regulation of the Energy and Mineral Resources (MEMR) No. 10/2025, which should regulate the roadmap for the phase-out of Coal-Fired Power Plants (CFPPs) to achieve the net-zero emission (NZE) target by 2060 or sooner, its implementation has not shown concrete progress. While Minister of…

Jakarta, November 20, 2025 - By the end of 2025, Indonesia’s energy transition remains largely rhetorical and continues to fall short of its stated goals. Although commitments to renewable energy appear to have strengthened over the past decade, the dominance of fossil fuels has in fact increased, further deepening the country’s dependence on fossil-based energy…

Background

Indonesia’s coal-producing regions—such as East Kalimantan and South Sumatra—have long relied on fossil fuel extraction as a major source of income and employment. However, as global and national commitments to carbon neutrality accelerate, these regions face the dual challenge of sustaining economic growth while phasing-down coal dependence. A just and inclusive economic transformation is…

Samarinda, October 15, 2025 - Synchronization among actors is the main key to encouraging a just energy transition, accompanied by strengthening human resource capacity. This capacity building is not limited to technical skills but also includes the ability to develop an entrepreneurial spirit. In this way, the energy transition can be realized equitably and provide…

Palembang, September 16, 2025 - South Sumatra (Sumsel) has long been known as one of Indonesia's energy hubs. Its natural resources, including coal, oil, and natural gas, make the province a key contributor to the national energy supply. However, amid the growing climate crisis, reliance on fossil fuels can no longer be a long-term…

Yogyakarta, June 4, 2025 – The energy transition to renewable sources is key to reducing Indonesia's dependence on coal while promoting a sustainable economy. At the Public Seminar "Coal Policy Reform," organized by the Institute for Essential Services Reform (IESR) in collaboration with the British Embassy in Jakarta through the Green Energy Transition Indonesia…

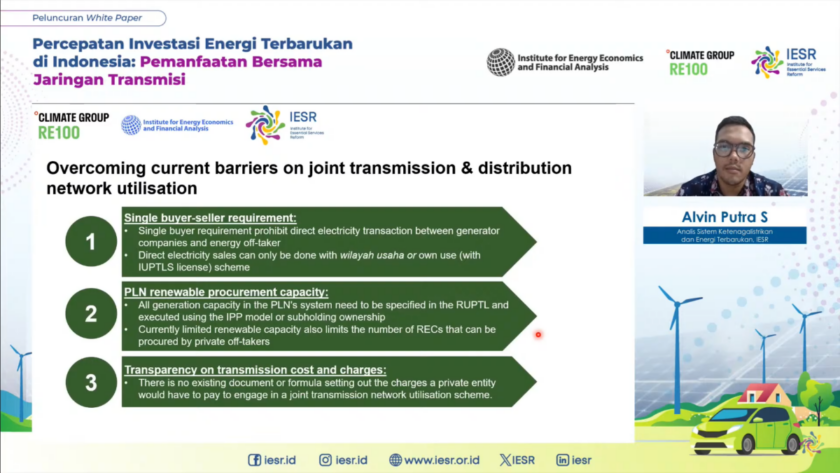

Jakarta, April 29, 2025 - Indonesia has renewable energy potential reaching more than 3,600 GW, but only around 0.3% of this renewable energy potential has been utilized. In the webinar " Accelerating Renewable Energy Investment in Indonesia: Shared Utilization of Transmission Networks ", for the launch of the white paper Accelerating Renewable Energy Investment…

Jakarta, April 16, 2025 - Energy security that supports emissions reduction must become a primary focus in developing cross-border electricity connectivity projects across the ASEAN region through the ASEAN Power Grid (APG). Highlighting Malaysia’s leadership as ASEAN Chair this year and its commitment to finalize the updated APG Memorandum of Understanding (MoU), the Institute for…

During the G20 Summit in Rio De Janeiro in November, Indonesia’s new president, Prabowo Subianto, issued a bold statement: Indonesia will retire all coal-fired power plants within the next 15 years and build over 75 GW of renewable energy capacity by 2040. Read more on Eco Business.

President Prabowo is targeting the operation of coal-fired power plants or PLTUs to be completely stopped by 2040. The Institute for Essential Services Reform or IESR revealed ways to achieve this target. Read more on Kata Data.

Jakarta, 10 December 2024 - Mineral downstreaming is a strategic step taken by the Government of Indonesia to provide added value in optimizing the economic benefits of domestic mineral resources and supporting the energy transition towards net-zero emission (NZE). The downstream program has an important role in the management of critical minerals. There are 47…